Key Highlight

- For 15 years, Dream11 built what is arguably the most sophisticated sports fan data infrastructure in India — 250 million registered users, 10 million daily active users, 14 terabytes of behavioural data processed per day, and a dataset that told brands exactly which 22-year-old in Patna would choose Rohit Sharma as captain five minutes before a match started. That data layer, built on the back of paid fantasy contests, transformed fantasy sports from a gaming product into India’s most valuable sports audience targeting platform.

- In August 2025, Parliament passed the Promotion and Regulation of Online Gaming Act, banning all real-money gaming including paid fantasy sports. Dream11 paused paid contests overnight. The ban erased an estimated ₹15,000 Crore from IPL advertising revenue alone — approximately 25% of the league’s total ad pie — and removed ₹1,500 Crore annually from Indian sports sponsorship budgets (Elara Capital; industry estimates). The commercial architecture that fantasy sports had built underneath Indian cricket’s economics collapsed in a single legislative session.

- Dream11 did not disappear. It pivoted. The company now operates a free-to-play fantasy platform with 10 million daily active users (as of September 2025), has split its parent Dream Sports into eight semi-autonomous startups (including Dream Sports AI, dedicated to analytics and fan engagement), and is repositioning as a “sports entertainment and analytics platform” rather than a gaming company. Brands like Swiggy, Tata Neu, and Astrotalk are already advertising on the free-to-play platform using the same engaged, demographically verified audience Dream11 built under its paid model.

- This blog is a comprehensive analysis of what Dream11’s data model actually was, how fantasy sports data reshaped Indian sports sponsorship for a decade, what the RMG ban has permanently changed, and — most importantly — what the playbook now looks like for brands targeting sports audiences, leagues rebuilding their sponsorship pipelines, and athlete managers navigating a commercial landscape that has fundamentally shifted since August 2025.

Table of Contents

- The Data Engine: What Dream11 Actually Built Over 15 Years

- How Fantasy Data Changed Sports Sponsorship — The Pre-Ban Model

- The Numbers That Made Dream11 Irreplaceable to Brands

- The RMG Ban: ₹15,000 Crore Gone in One Legislative Session

- The Sponsorship Vacuum: Who Fills ₹1,500 Crore of Annual Sports Funding?

- Dream11’s Pivot: From Gaming Giant to Sports Analytics Platform

- Dream Sports AI and the Data Asset That Survived the Ban

- The Free-to-Play Fantasy Model: What It Means for Brand Sponsorship

- What This Means for Leagues and Sports Properties

- What This Means for Athlete Managers

- The New Sponsorship Playbook: What Fills the Fantasy Gap

- FAQ: Fantasy Sports Sponsorship Data India

- The Data Layer Doesn’t Disappear — It Just Changes Owners

The Data Engine: What Dream11 Actually Built Over 15 Years {#data-engine}

To understand what was lost — and what survives — when paid fantasy sports was banned, you first need to understand what Dream11 actually was, underneath the fantasy cricket branding.

Dream11 was not primarily a gaming company. It was a sports fan data company that used fantasy gaming as its user acquisition mechanism.

The fantasy game was the front door. The back-end was a data infrastructure that, by any benchmark, is extraordinary. Dream11 processed 14 terabytes of behavioural data per day through a homegrown analytics platform it began building in 2017 as a “data highway.” This system tracked hundreds of types of user behaviour in near real time: which player a user selected as captain, how long they deliberated before finalising a team, which contests they joined and abandoned, what their historical selection patterns revealed about their cricket knowledge level, which match formats (Test, ODI, T20) drove their highest engagement, and which players they consistently overvalued or undervalued relative to the broader user population.

By 2025, Dream11 had accumulated 250 million registered users — all verified with PAN and identity documentation (a legal requirement for cash-based gaming), all of whom had demonstrated active sports engagement through repeated voluntary participation in contests requiring genuine cricket knowledge. Dream Sports CEO Harsh Jain described the data orientation precisely: “Every decision we make is backed by data and technology, considering various metrics to continually add ‘wow factors’ that help retain customers.” The platform’s ML models forecast contest demand, detect fraud, and personalise which of the hundreds of simultaneously running contests are recommended to each user based on their historical behaviour.

This was not passive demographic data — the kind a broadcaster collects from viewership logs. It was active engagement data: proof of intent, demonstrated knowledge, and revealed preference at the individual user level. A user who has played 200 Dream11 contests over three years is identifiable as a specific type of cricket fan — high-knowledge, specific team allegiance, specific player preferences, specific match format preference — in a way that is impossible to determine from broadcast viewership records, social media follows, or survey data.

That is the data asset Dream11 built. And for a decade, it was the most commercially powerful fan targeting infrastructure in Indian sports.

How Fantasy Data Changed Sports Sponsorship — The Pre-Ban Model {#pre-ban-model}

Before Dream11 became India’s largest sports sponsor in its own right, it transformed how other brands approached sports sponsorship by creating a targeting layer that had never previously existed in Indian sports media.

The traditional sports sponsorship model is essentially broadcast-based audience buying. A brand pays for jersey placement or stadium branding, the match airs on a broadcaster with a reported viewership number, and the brand assumes its logo received proportional exposure. The audience data underlying this assumption is, at best, an estimated demographic profile from third-party research. At worst, it is simply a viewership number with no demographic depth — a count of eyeballs, not a profile of people.

Fantasy sports introduced a different targeting layer alongside broadcast. Dream11’s user data allowed brands to reach sports fans not through assumed exposure during a broadcast but through verified, profiled, self-selected interaction. A fan who is actively selecting Jasprit Bumrah as their bowling pick for tonight’s match is demonstrably more engaged with that specific player than a fan who is watching the same match passively from their sofa. The engagement gap is not marginal. Research consistently shows that fantasy sports participants demonstrate 40–60% higher live match attendance rates, higher merchandise purchase rates, and significantly higher recall of brand placements compared to non-fantasy-sports viewers.

Dream11 monetised this attention gap in two distinct ways. First, it sold advertising on its own platform — in-app placements, contest integrations, and branded content visible to authenticated users during their highest-engagement sports moments. Second, it anonymised and aggregated its user data to offer brands targeted insights about sports audiences that no broadcaster could provide: the demographic and behavioural profile of India’s most engaged cricket fans, segmented by team allegiance, player preference, geographic distribution, and contest-participation intensity.

The result was a three-tier commercial architecture that Dream11 occupied simultaneously: as a gaming platform (generating revenue from contest entry fees), as an advertising platform (selling targeted access to verified sports audiences), and as a data intelligence platform (providing brands with audience insights to optimise their broader sports marketing spend beyond Dream11’s own properties).

This three-tier architecture is what made Dream11’s commercial value to the Indian sports ecosystem far larger than its own revenue figures suggested. It was not just a sponsor — it was the targeting intelligence layer that made other sports sponsorships more efficient.

The Numbers That Made Dream11 Irreplaceable to Brands {#numbers}

The commercial scale Dream11 reached before the ban is important context for understanding why the August 2025 legislation had such an immediate and severe impact on Indian sports sponsorship.

Dream11 spent approximately ₹5,700 Crore on advertising over six years — an average of ₹950 Crore per year in advertising spend that flowed directly into sports broadcast revenue, sports content creation, and athlete endorsements. Its 2020 IPL title sponsorship cost ₹222 Crore. Its lead jersey sponsorship of the Indian national cricket team from 2023 to 2026 was ₹358 Crore. It held jersey sponsorship rights with five IPL franchises simultaneously. By 2024, Dream11 and its direct RMG competitors (My11Circle, WinZO) collectively contributed approximately 25% of IPL’s total advertising revenue.

The demographic quality of Dream11’s user base made this advertising spend extraordinarily efficient for brands: 70% of Dream11’s registered users were aged 18–35, the highest-value demographic for virtually every consumer brand category. These users were not passive — they had demonstrated purchase intent through their willingness to pay real money for sports contests, a transaction that is a high-confidence signal of disposable income and discretionary spending capacity.

My11Circle’s commitment of ₹625 Crore over five years for IPL fantasy rights reflected the same commercial logic. For every crore invested in the IPL fantasy ecosystem, RMG platforms received access to the most engaged, demographically verified sports audience in India. The IPL franchise system, in turn, used fantasy platform sponsorship fees to fund team operations, player salaries, and production — creating a financial interdependency that ran through every layer of Indian cricket’s commercial structure.

At the non-cricket level, RMG companies invested more than ₹1,500 Crore annually in sports sponsorship beyond cricket — funding Pro Kabaddi League, Hockey India League, badminton leagues, and esports events that had limited alternative commercial backing. This was the invisible subsidy that sustained India’s non-cricket sports commercial ecosystem for nearly a decade.

The RMG Ban: ₹15,000 Crore Gone in One Legislative Session {#rmg-ban}

On August 22, 2025, Parliament passed the Promotion and Regulation of Online Gaming Act. The legislation banned all “online money games” — any digital game where players stake money in exchange for a chance to win cash. The definition explicitly covered fantasy sports regardless of the skill component, overriding the judicial precedents that had previously protected Dream11’s “game of skill” classification.

Dream11 CEO Harsh Jain confirmed in an interview with Moneycontrol that paid contests accounted for roughly 95% of the platform’s revenue and 100% of its profits. Dream11 paused all paid contests within days of the Act’s passage. My11Circle, MPL, WinZO, and other RMG platforms followed. The India tour of England during Asia Cup 2025 saw the Indian cricket team play without a jersey sponsor — an image that captured the commercial disruption more viscerally than any financial report.

Elara Capital’s analysis quantified the immediate damage: the RMG industry’s 25% share of IPL advertising revenue — approximately ₹15,000 Crore — was effectively removed from the broadcaster’s inventory. JioStar, already managing ₹25,760 Crore in provisions for onerous sports contracts, faced a simultaneous hit to its advertising revenue base. The digital advertising industry’s growth rate was projected to moderate by 300 basis points as a direct consequence.

The broader sports sponsorship impact extended beyond IPL. RMG companies had been the most aggressive bidders for sponsorship inventory across every major Indian sports property. Their exit created a structural vacuum at the top of the Indian sports sponsorship market at the precise moment that several non-cricket leagues were depending on that capital to build financial sustainability.

For GSK’s sponsorship and media rights practice, the August 2025 legislation was the single most consequential commercial event in Indian sports since the 2022 IPL media rights auction — and its full commercial implications are still being absorbed by leagues, brands, and broadcast partners through 2026.

The Sponsorship Vacuum: Who Fills ₹1,500 Crore of Annual Sports Funding? {#sponsorship-vacuum}

The ₹15,000 Crore IPL advertising impact was the headline number. The ₹1,500 Crore annual non-IPL sports sponsorship vacuum is the figure with more structural long-term significance for Indian sports development.

RMG platforms were, for much of the last decade, the primary commercial backers of non-cricket Indian sports properties. PKL, HIL, badminton leagues, and emerging esports tournaments depended on fantasy gaming sponsorship fees that reflected a specific commercial logic: RMG users over-index on sports engagement, making sports properties the highest-ROI advertising channel for fantasy platforms regardless of whether the sport is cricket, kabaddi, or hockey. A Fantasy Sports fan who has never played kabaddi is still an ideal advertisement target for a kabaddi fantasy contest — the sport just needs to be represented on the platform.

With that commercial logic removed by the ban, non-cricket Indian sports lost a category of sponsor that had underwritten much of the growth in Indian sports sponsorship over the preceding five years. Grassroots programs funded by Dream Sports Foundation, youth academies supported through fantasy platform partnerships, and state-level tournaments whose commercial models were built around fantasy gaming sponsorship all faced simultaneous funding compression.

The replacement sponsors are emerging, but they represent a different kind of commercial relationship. Elara Capital’s analysis identified e-commerce platforms, consumer tech brands, fintech apps, and consumer goods companies as the most likely candidates to fill the IPL advertising vacuum — attracted by the lower ad rates that result from reduced competitive bidding now that the aggressively spending RMG category has exited. Apollo’s sponsorship of the Indian national cricket team jersey (replacing Dream11’s exited deal) exemplifies this shift: a consumer healthcare brand with none of the regulatory risk that defined RMG sponsorships, offering a more stable long-term commercial partnership with less volatility.

For leagues and sports properties negotiating sponsorship deals in 2026, the core commercial implication is that the replacement sponsors have different audience requirements than RMG platforms did. Fantasy platforms needed broad sports fan reach with demographic weighting toward 18–35-year-old males. FMCG brands, consumer tech companies, and fintech platforms need more specific audience profiles — particular demographics, income brackets, and purchasing behaviours that go beyond “watches cricket.” This shift increases the commercial premium on sports properties that can provide verified audience data: the leagues and clubs that built first-party fan data infrastructure (as discussed in our sports OTT strategy guide) can articulate their audience quality to these more selective sponsors.

Dream11’s Pivot: From Gaming Giant to Sports Analytics Platform {#pivot}

Dream11’s response to the ban has been strategically coherent, commercially ambitious, and — by the metrics available — more successful at maintaining user engagement than most industry observers expected.

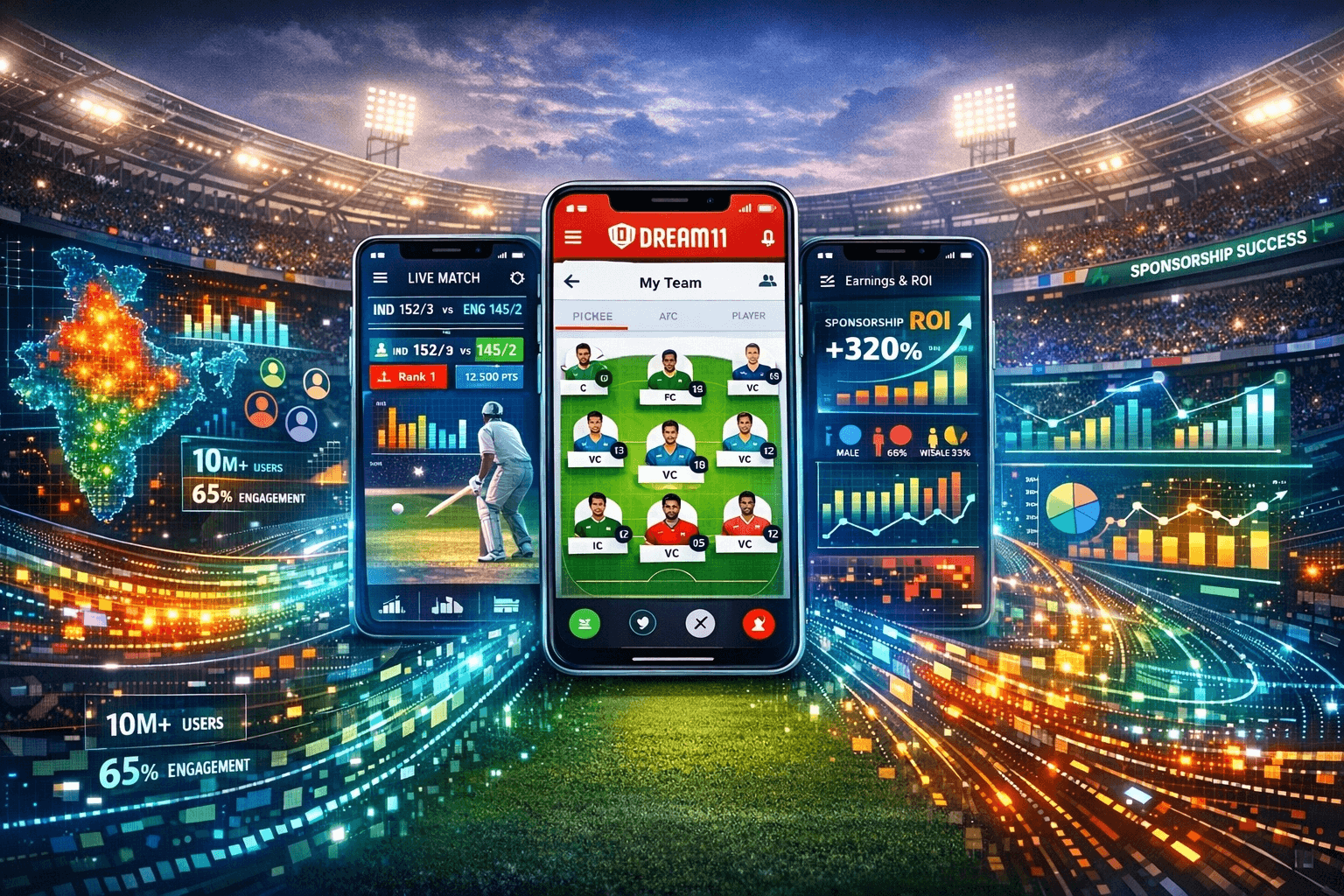

Within weeks of the ban, Dream11 relaunched as a free-to-play platform. Users can continue creating fantasy teams and competing in daily contests, with prizes now provided by brand sponsors rather than pooled cash entries. By September 2025, the free-to-play platform had attracted 10 million daily active users — a number that, while significantly below the paid contest peak, represents a substantial engaged audience for advertising purposes. Crucially, 70% of those users remain in the 18–35 age bracket, and the platform retains access to the historical transaction and behavioural data accumulated from users’ years of paid participation.

Dream Sports simultaneously restructured itself into eight semi-autonomous business units, a reorganisation that explicitly separates the company’s future commercial engines from the now-dormant paid gaming model:

- Dream11 — free-to-play fantasy and second-screen sports entertainment

- FanCode — sports content streaming and niche rights distribution

- Dream Sports AI — analytics, prediction tools, and AI-driven fan engagement products

- DreamSetGo — premium sports travel and fan experience management

- Dream Cricket — mobile gaming (non-cash)

- Dream Money — fintech and micro-investing

- Dream Horizon — technology infrastructure for developers

- Dream Sports Foundation — social impact and grassroots development

The commercial significance of this restructuring, for anyone tracking the Indian sports industry, is the explicit creation of Dream Sports AI as a dedicated analytics and data intelligence unit. Dream11’s 15 years of sports fan behavioural data — 250 million registered profiles, years of team selection patterns, contest participation histories, demographic verification — does not disappear when paid contests are banned. It migrates into the analytics infrastructure that Dream Sports AI is being built to commercialise through brand partnerships, league data licensing, and sports intelligence products.

Dream Sports AI and the Data Asset That Survived the Ban {#dream-sports-ai}

The most under-reported consequence of the RMG ban for Indian sports sponsorship is that Dream11’s data infrastructure is not only intact — it is being actively invested in as the company’s primary future commercial engine.

Dream Sports AI’s mandate, as described in the Dream Sports restructuring announcement in December 2025, covers analytics, prediction tools, and AI-driven fan engagement products. The commercial applications of this capability in a sports sponsorship context are direct:

Player performance prediction modelling. Dream11’s fantasy selection data is the largest revealed-preference dataset on Indian cricket performance prediction in existence. When 10 million active users make team selection decisions before each match, they are collectively producing a real-time, crowd-sourced performance forecast — one that aggregates the cricket knowledge of India’s most engaged fans. This data, properly modelled, provides player performance predictions of a kind that traditional analytics approaches (based on historical match statistics alone) cannot replicate, because it incorporates millions of data points of expert fan judgment made under conditions of real incentive (previously real money, now contest prizes).

Audience segmentation for sports sponsorship. The brand advertising model Dream11 has pivoted to — Swiggy, Tata Neu, and Astrotalk integrating into contests as sponsors — depends on the same audience segmentation capability that made Dream11’s advertising valuable under the RMG model. The user data exists, the segmentation tools exist, and the commercial product is the same: brands pay for access to specific, verified segments of Dream11’s engaged user base, targeted based on demographic and behavioural profiles built from years of fantasy participation.

Cross-property audience intelligence through FanCode. The Dream Sports ecosystem now combines Dream11’s fan behaviour data with FanCode’s content consumption data (FanCode has 100 million users with verified profiles, streaming non-cricket sports including Formula 1, La Liga, ISL, and emerging properties). This cross-property data creates an audience intelligence capability that is broader than either platform individually — a sports fan profile that incorporates both gaming engagement and content consumption, covering cricket and non-cricket sport, urban and Tier-2/3 demographics.

For brands thinking about how to use sports analytics for sponsorship decision-making, the Dream Sports AI ecosystem represents a data intelligence resource whose value to Indian sports sponsorship targeting has not diminished with the RMG ban — it has simply changed its commercial packaging.

The Free-to-Play Fantasy Model: What It Means for Brand Sponsorship {#free-to-play}

Dream11’s free-to-play pivot introduces a new sponsorship format that brands are only beginning to understand: the branded contest.

Under the paid model, brands advertising on Dream11 were buying media placement — in-app banners, pre-match notifications, and splash screens on a platform where users were highly engaged but the engagement was primarily financial (winning money) rather than brand-oriented. Brand recall in this environment was real but incidental — the platform’s primary value was the engaged audience, and the brand’s visibility was adjacent to that engagement.

Under the free-to-play model, brands become the prize mechanism. A Swiggy-branded contest offers ₹500 food vouchers as prizes. A Tata Neu-branded contest offers NeuCoins. An Astrotalk contest offers premium consultation credits. The brand is not an advertisement adjacent to the game — it is structurally embedded in the game’s reward architecture. Users who win a Swiggy contest must redeem their prize through Swiggy, creating a direct conversion path from fantasy engagement to brand transaction that the paid model could not provide.

Dream Sports CMO Vikrant Mudaliar articulated the commercial proposition precisely: “This reimagining makes fantasy sports more inclusive and passion-driven, while giving advertisers quality reach and measurable engagement, and access to a very rich audience of historically transacting users.” The key phrase is “historically transacting users.” Dream11’s advertising proposition to brands is not just current free-to-play engagement — it is access to an audience whose years of paid participation have produced verified evidence of their willingness to spend money on sports-adjacent products, which is a commercial signal that no other sports audience platform in India can offer.

For brands evaluating whether to allocate sports sponsorship budgets to Dream11’s free-to-play platform post-ban, the key metric shift is from passive impression volume (how many people saw the ad) to active engagement rate (how many people interacted with the branded contest, claimed the prize, and completed a transaction with the sponsoring brand). The Dream Sports ecosystem, with sports marketing analytics supporting the measurement architecture, can provide conversion-based ROI metrics that traditional sports broadcast sponsorship cannot.

What This Means for Leagues and Sports Properties {#leagues}

The RMG ban’s impact on leagues and sports properties operates at two distinct levels: the immediate commercial impact of losing RMG sponsorship fees, and the structural shift in what sponsor categories are available as replacements.

The immediate commercial impact is most acute for non-cricket leagues that had built commercial models with significant RMG dependence. PKL, HIL, and badminton leagues all had fantasy platform partnerships that contributed to their sponsorship revenue. The exit of these sponsors in August 2025 created immediate funding gaps that state-level leagues and grassroots programs are still absorbing. For new leagues like CHL 2026, the commercial environment they are entering has fewer high-spend sponsors competing for niche sports inventory — but it also has lower sponsorship pricing expectations from the remaining sponsors, which affects rights valuation.

The structural shift in sponsor categories is more nuanced and ultimately more constructive for leagues with strong audience data. RMG sponsors needed broad sports fan reach because fantasy platform ROI was driven by user volume — more sports fans meant more potential fantasy contest participants. FMCG, consumer tech, and fintech sponsors have more specific audience requirements. They want sports properties whose fan demographics match their target customer profile, not simply the largest sports audience available.

This shifts the commercial advantage toward leagues with documented, verified fan audiences — properties that can tell a potential sponsor “our audience is 65% aged 22–38, 58% from Tier-2 and Tier-3 cities, with average household incomes above ₹8 Lakh per year” rather than simply claiming large viewership numbers. The events and tournaments management that produces these audience data assets — match day registration, digital ticketing with demographic capture, streaming with authenticated access — is the infrastructure that creates the sponsorship proof that post-RMG sponsors will require.

For emerging leagues specifically, the CHL 2026 model — which combines government VGF funding (₹3.5 Crore) with franchise fees (₹9 Crore) rather than RMG sponsorship dependence — is precisely calibrated for the post-ban environment. Leagues that built their financial models around RMG sponsorship fees are now restructuring toward more diversified revenue bases. Leagues designed from the outset with government partnerships, franchise economics, and first-party fan data infrastructure are in a structurally stronger position than the post-ban landscape might initially suggest.

What This Means for Athlete Managers {#athlete-managers}

For athlete managers, the RMG ban’s impact on personal endorsement markets is more nuanced than the sponsorship vacuum at the league level — and contains both negative and positive signals that require careful commercial navigation.

The negative signal is direct. Fantasy sports platforms were, for Indian athletes outside the top tier, a significant source of endorsement income. Dream11’s “Dimaag se Dhoni” campaign model — featuring seven cricketers simultaneously in its 2019 IPL campaign — represented a template of athlete endorsement spending that non-A-list cricketers and non-cricket athletes benefited from. Fantasy platforms needed large rosters of recognisable athletes for their marketing; they were willing to pay endorsement fees to players who would not attract FMCG or tech brand attention. The exit of this spending category removes a meaningful commercial option from the endorsement market for athletes ranked 15–100 in their sport’s commercial hierarchy.

The positive signal is more structural. Fantasy sports data was one of the first commercial tools that revealed the genuine commercial value of non-cricket athletes to Indian brands. When Dream11’s contest data showed that PKL stars like Pawan Kumar Sehrawat generated higher fantasy team selection rates than some second-tier cricketers — and that kabaddi-specific fantasy contests retained users at comparable engagement rates to cricket contests — it produced quantified evidence of athlete commercial value that the traditional endorsement market had not previously captured.

That data intelligence is now part of Dream Sports AI’s commercial portfolio, and it is the kind of audience engagement data that athlete management firms increasingly need to negotiate endorsement deals on behalf of non-cricket athletes. An athlete manager who can show a brand “your target audience — 25–35-year-olds in Hindi-belt cities — selected this kabaddi player in 2.3 million Dream11 teams last season” is in a different commercial conversation than one who can only cite audience reach and social media followers.

The RMG ban removed the fantasy platform category as a direct endorsement client. What it left behind is a data infrastructure that quantifies athlete commercial value in ways that benefit athletes and their managers across all other endorsement categories — if those data assets are properly accessed and commercially deployed.

The New Sponsorship Playbook: What Fills the Fantasy Gap {#new-playbook}

For brands previously using fantasy sports data to target sports audiences, the post-ban environment requires a new playbook. For brands that are new to sports sponsorship and are now entering a market where advertising inventory has become more affordable (because aggressive RMG bidders have exited), the environment presents a genuine opportunity.

Here is how the categories of replacement sponsors are positioned:

| Sponsor Category | Why They Replace RMG | Audience Fit | Commercial Model |

|---|---|---|---|

| E-commerce (Flipkart, Meesho, Nykaa) | Broad reach; IPL ad rates cooling post-ban | 18–40 urban and semi-urban consumers | Impression + conversion tracking |

| Consumer tech (Jio, realme, OnePlus) | Mass reach; young male-skew audience | 18–35 mobile-first consumers | Brand awareness + product launches |

| FMCG & beverage (Parle, Dabur, Tata Tea) | Brand recall; mass market reach | 25–50 family-decision-makers | Reach + occasion association |

| Fintech (Zerodha, Groww, Paytm) | Post-RMG vacuum at same price points | 22–38 financially active users | Verified audience with spending history |

| Healthcare & wellness (Apollo, Himalaya) | Brand legitimacy in sports context | 30–50 health-conscious consumers | Trust + brand association |

| EdTech & upskilling (BYJU’S revival, Coursera) | Sports audience for aspirational marketing | 18–30 students and early career | Aspiration + conversion |

For leagues looking to replace RMG sponsors, the commercial argument is not simply “we have the same audience.” It is “we have the same audience, with better demographic data, at lower ad rates than were available when RMG sponsors were competing aggressively.” The post-ban pricing correction at IPL and other cricket properties makes sports sponsorship more accessible to brand categories that were previously priced out by the competitive RMG bidding environment.

For non-cricket leagues, the calculus is more complex. RMG sponsors were willing to back niche sports because niche sports fans were also fantasy platform users. Consumer brands are more selective. A kabaddi league in an industrial state needs to demonstrate that its audience profile matches what a fintech or FMCG brand specifically needs — which requires the kind of audience data infrastructure that, as of 2026, very few non-cricket sports properties in India possess.

Building that audience data infrastructure — and turning it into the commercial evidence that post-RMG sponsors require — is the core commercial challenge and opportunity for Indian sports properties in the next 24 months.

FAQ: Fantasy Sports Sponsorship Data India {#faq}

Q: How did Dream11’s fantasy sports data directly influence sports sponsorship decisions in India?

Dream11’s 250 million registered users generated behavioural data — team selection patterns, player preference histories, contest participation frequency, geographic distribution, and demographic profiles — that was more commercially specific than any broadcast viewership data. Brands advertising on Dream11 could reach sports fans segmented by player allegiance, team preference, geographic location, and engagement intensity. Fantasy participation is a proxy for purchasing intent: users who have historically paid real money to engage with sports are a commercially verified audience in a way that passive viewers are not. Dream11 also used this data to inform its own sponsorship spending — the sports properties it invested in were selected based on where its user base showed the highest engagement, creating a data-feedback loop that shaped Indian sports sponsorship allocation for a decade.

Q: What is the Promotion and Regulation of Online Gaming Act 2025 and how did it affect sports sponsorship?

The Act, passed by Parliament in August 2025, banned all “online money games” — digital games where players stake money in exchange for a chance to win cash. This directly outlawed paid fantasy sports contests, forcing Dream11, My11Circle, MPL, and WinZO to halt real-money operations. The commercial impact on Indian sports was immediate: RMG companies removed approximately ₹15,000 Crore from IPL advertising revenue (approximately 25% of the league’s total ad pie) and ₹1,500 Crore from annual non-cricket sports sponsorship. The Act preserves esports and free-to-play fantasy sports, which is the regulatory space Dream11 now operates in with its free-to-play pivot.

Q: Is Dream11 still operating in 2026? What happened after the ban?

Dream11 still operates in India, but without paid contests. The platform shifted to a free-to-play model from August 2025, where users compete for brand-sponsored prizes (Swiggy vouchers, Tata Neu credits) rather than cash. As of September 2025, the free-to-play platform had 10 million daily active users with 250 million registered accounts. Dream Sports, the parent company, simultaneously restructured into eight business units including Dream Sports AI (analytics and fan engagement) and continued to operate FanCode (sports content streaming), DreamSetGo (sports travel), and other portfolio companies. Dream11’s BCCI jersey sponsorship ended as a consequence of the ban; Apollo became the Indian cricket team’s new jersey sponsor.

Q: What does the RMG ban mean for non-cricket sports league sponsorship in India?

Non-cricket leagues lost a category of sponsor that had been commercially critical: RMG platforms invested ₹1,500 Crore annually in non-cricket sports sponsorship. This funding subsidised PKL, HIL, badminton leagues, and emerging sports leagues whose commercial models were partially or significantly dependent on fantasy platform fees. The replacement sponsors — FMCG, consumer tech, fintech — are more selective about audience requirements, creating a commercial premium on sports properties with verified demographic data. Leagues that can demonstrate audience quality through first-party fan data are in a stronger position to attract replacement sponsors than leagues that only have viewership numbers. New leagues designed without RMG dependence — using franchise models, government partnerships, and diversified revenue — are structurally better positioned for the post-ban environment.

Q: How can athlete managers use fantasy sports data in endorsement negotiations today?

While Dream11’s paid platform no longer generates live fantasy data, the historical dataset from 250 million users making team selections across millions of contests represents the most granular measure of athlete commercial appeal to India’s engaged sports fan base that exists. Dream Sports AI is commercialising this data through analytics products. Athlete managers should understand that an athlete’s historical Dream11 selection rate — how frequently fans chose them for fantasy teams relative to their peers — is a quantified measure of audience affinity that translates directly to endorsement ROI arguments with consumer brands. An athlete with a high fantasy selection rate has demonstrably captivated the attention of India’s most commercially active sports fans; that is the core argument for endorsement value, and it can now be documented rather than assumed.

Q: Will paid fantasy sports return to India? What is the current regulatory status?

As of March 2026, paid fantasy sports remain banned under the Online Gaming Act 2025. Dream11 CEO Harsh Jain stated publicly that the company will not challenge the Act legally. The Act does permit “online games of skill” including esports, distinguishing them from “online money games.” Several legal challenges to the Act from industry bodies are expected, citing constitutional questions about state vs. central jurisdiction over gambling regulation (gambling is constitutionally a state subject). While the legal landscape may evolve, Dream11 has committed to its free-to-play model for the foreseeable future and is building commercial infrastructure that does not depend on a regulatory reversal.

The Data Layer Doesn’t Disappear It Just Changes Owners

India’s fantasy sports ecosystem built the most powerful sports fan targeting infrastructure the country has ever had — and then lost the revenue model that funded it in a single legislative session.

That discontinuity is real, painful for the companies involved, and commercially significant for the sports properties and athlete managers who depended on RMG sponsorship income. But the data layer that Dream11 built does not disappear when paid contests are banned. It migrates into Dream Sports AI, into FanCode’s content analytics, into the free-to-play platform’s brand integration model, and into the commercial intelligence products that the restructured Dream Sports ecosystem is building.

What changes is not the existence of fantasy sports data — it is who benefits from it, on what terms, and in what commercial format. Under the paid model, brands benefited from Dream11’s data primarily as an advertising targeting layer. Under the post-ban model, brands benefit from Dream11’s data through branded contest integrations, audience intelligence products, and the cross-platform engagement metrics that Dream Sports AI is building into the FanCode + Dream11 ecosystem.

For leagues, the departure of RMG sponsors creates a genuine commercial gap — but also an opportunity to replace a highly volatile, regulatory-risk-concentrated sponsor category with more stable, long-term partners from FMCG, consumer tech, and fintech. The leagues that build their own audience data infrastructure rather than relying on RMG platforms to provide audience targeting for their sponsors will be better positioned in this new environment than those who try to replace Dream11 sponsorship like-for-like.

For athlete managers, the fantasy data infrastructure that quantified athlete commercial value remains accessible — as an analytics product rather than a live platform — and is increasingly the evidentiary foundation for endorsement negotiations in a post-RMG market where brands are more selective about what audience they are actually reaching.

GSK’s sponsorship and media rights advisory, sports analytics capabilities, and sports marketing strategy practice are all informed by the structural shift the RMG ban has created in Indian sports commercials. Understanding how to fill the sponsorship gap, build the audience data infrastructure that post-RMG sponsors require, and use emerging analytics tools to quantify athlete and event commercial value is the commercial challenge and opportunity that defines Indian sports sponsorship for the next three years.

To understand how GSK can help your league, sports property, or athlete management practice navigate this environment, reach us at info@globalsportskonnect.com or book an intro call. Follow our LinkedIn for weekly analysis of the evolving Indian sports business landscape.